Demystifying Arbitrage Funds

Arbitrage Funds have become all the rage over the last couple of years because of their debt-like returns but with equity-like taxation. Yet, few people fully understand how they operate and there’s significant confusion about what these funds are (or not) suitable for.

What are Arbitrage Funds?

Arbitrage Funds are a type of hybrid mutual fund that invest in both equity and debt. These aim to capture short-term interest rates in the market, without taking any directional market risk. Arbitrage Funds generate majority1 of their returns from Cash-and-Carry arbitrage trades, and from investing in money market instruments.

What are Cash-and-Carry arbitrage trades?

Normally, stock futures trade at a higher price than the underlying stocks. The price difference is primarily determined by the cost to borrow money until futures’ expiry, but also influenced by market demand-supply dynamics. Theoretically:

$$F = S \cdot (1 + r - d)^t$$

Where:

- F: Futures price

- S: Spot price

- r: risk-free rate

- d: dividends

- t: time to expiry

Arbitrage funds profit from this price difference by buying shares in the spot market and simultaneously shorting the futures. The two simultaneous trades allow arbitrage funds to capture the risk-free rate using equities. The trades are also economically hedged (or balanced), insuring them from market movements.

What are money-market instruments?

Money market instruments are low-risk, highly liquid, short-term debt securities, with maturities of one year or less. Examples include Treasury Bills, Commercial Paper, Certificates of Deposit, Repurchase Agreements (Repos), etc.

Arbitrage funds invest in money market directly by holding the underlying instruments, or indirectly by holding mutual funds that invest in money-market.

Returns

Arbitrage Funds’ returns can be expressed as:

Arbitrage returns = returns from equity trades + returns from money market investments

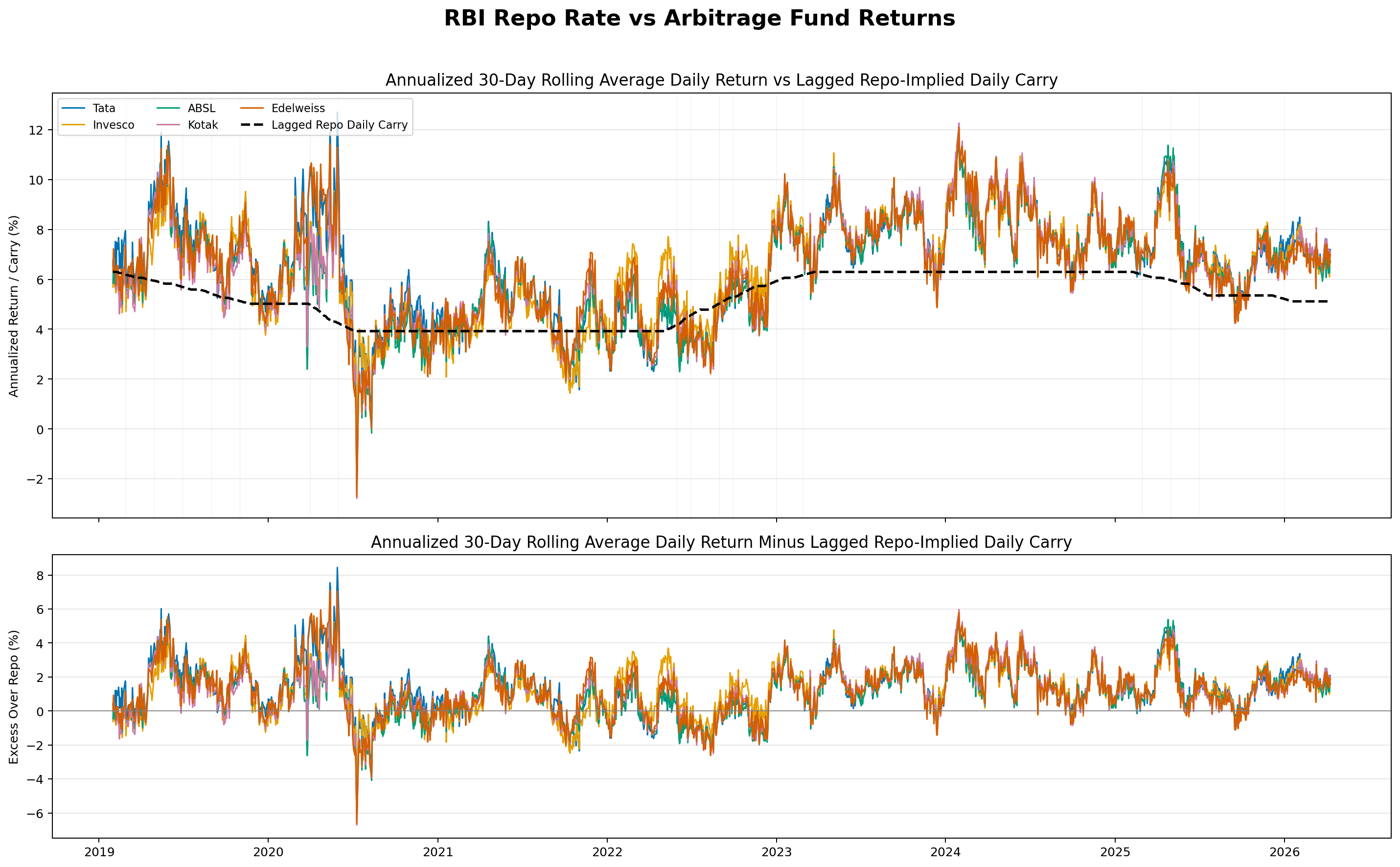

The risk-free rate in India (as determined by the repo rate set by RBI) closely affects both of these:

- The difference between the spot and futures price is primarily determined by the rate

- Money-market instruments carry a small credit risk on top of govt. bonds but the returns are closely tied to T-Bills.

The real-world returns from cash-and-carry trades are a little lower than the theoretical value mentioned earlier because of frictions:

returns from cash-and-carry trades = spread between futures and spot prices – (transaction costs + impact cost + taxes + slippage)

Risk/Safety Profile

If you look at SEBI riskometer of Arbitrage funds, they have the lowest risk rating, indicating their inherent safety. However, there are certain aspects that one should be aware of:

Basis Risk (short-term volatility)

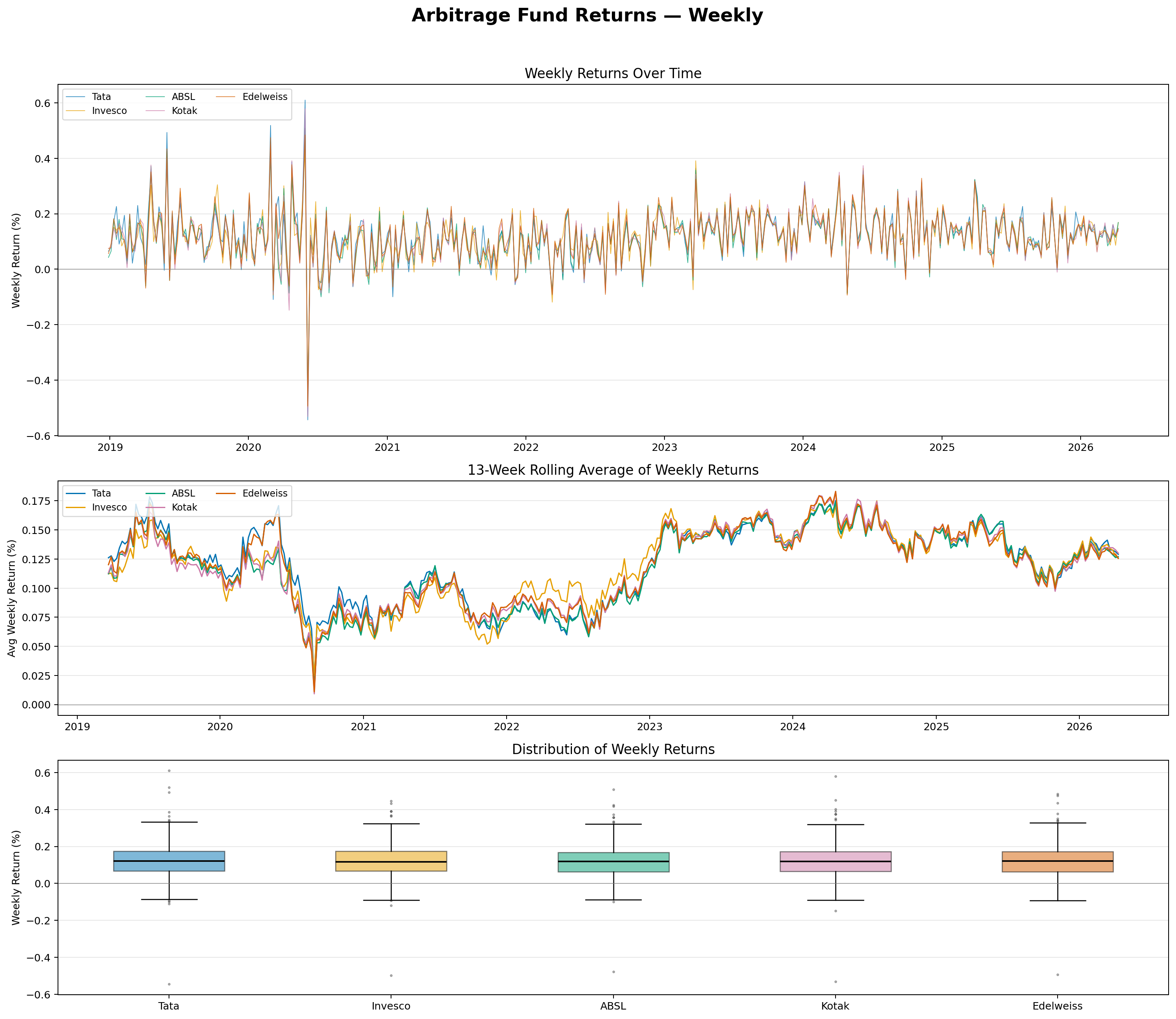

If you analyse the week-over-week change in the NAV of arbitrage funds, you will realise that these funds often provide zero or even slightly negative returns. This may seem surprising and scary but is also unavoidable.

This is because while the equity trades for an arbitrage fund are 100% hedged, sometimes the difference between the spot and futures can deviate too much from the expected during times of inflation or interest rate uncertainty. The demand (or lack there of) for futures push their prices too far, leading to fluctuations in the spreads. This can lead to a mark-to-market (MTM) or accounting loss for arbitrage funds, resulting in the lower NAV but at the time of futures expiry, the price divergence between spot and futures closes, and the paper loss recovers.

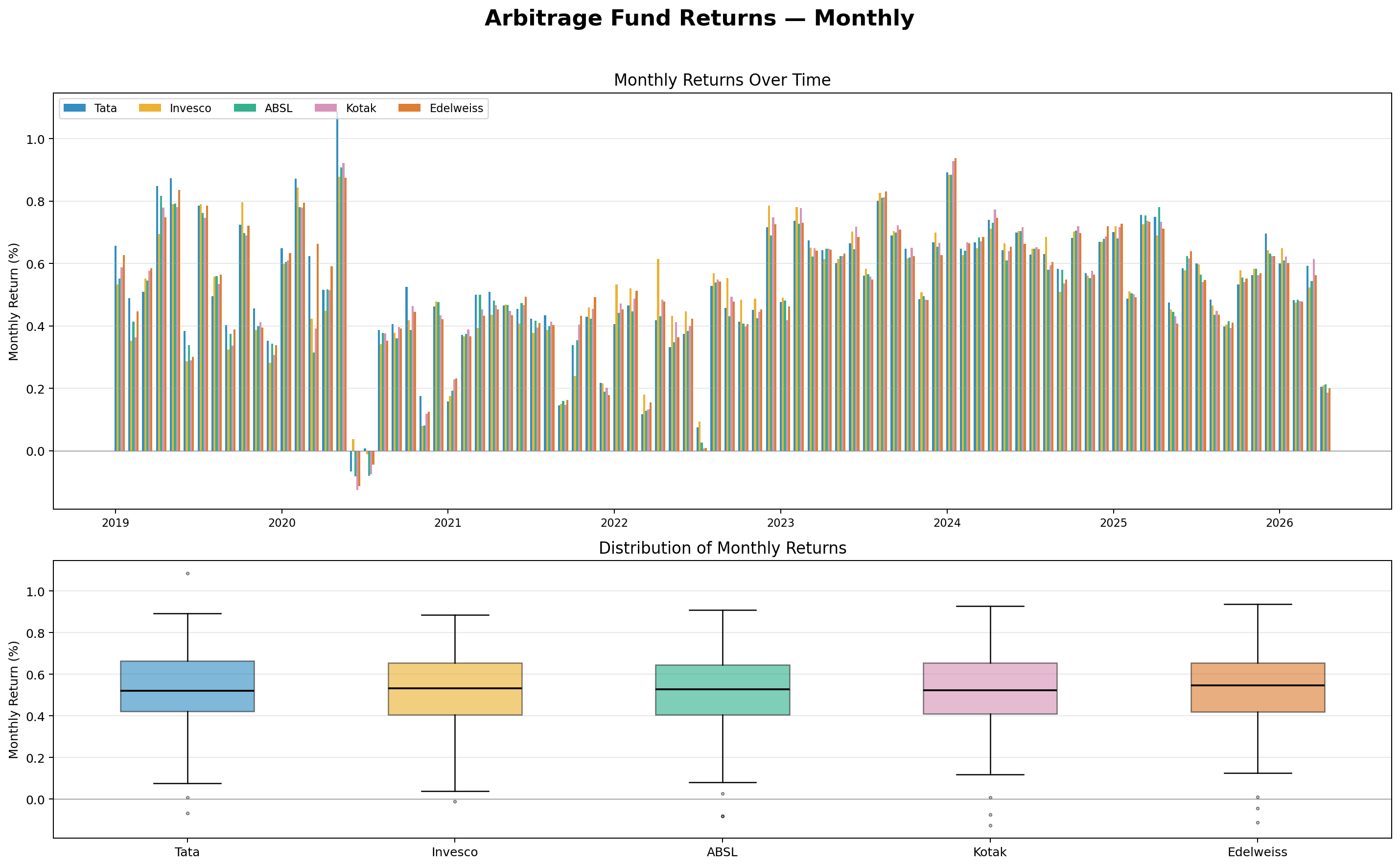

Since 2019, the earliest I could pull the data for:

- The month-on-month returns have always been positive, except the Covid 2020 crash, which resulted in ~ -0.1% returns.

- the rolling returns over longer duration (13 weeks or ~3 months or), present a much less picture bleak than rolling 1-week returns.

The longer periods allow enough futures cycles to play out, averaging the impact of temporary fluctuations.

Liquidity/Impact Cost Risk

If an arbitrage fund uses low liquidity stocks as the underlying, its returns can be more muted than expected. This is because when the fund tries to sell large volume of low-liquidity stocks, the selling can affect the price too much, lowering the returns.

This risk can be managed by:

- using a well-diversified portfolio of highly liquid stocks

- spreading the stock liquidation over a slightly longer duration

Duration and Credit Risk

The debt portion of arbitrage funds is supposed to be invested in high-quality paper, with low duration (interest rate risk). However, in order to boost returns, some fund managers turn to slightly lower-rated commercial paper, or use longer duration bonds.

This used to be a hidden risk in many funds but in February 2026, SEBI issued new guidelines 2 that limit Arbitrage funds to only invest in sovereign quality paper, under 1 year of maturity. These removed the possibility of a fund taking credit or too much duration risk, and have made the entire category safer by default.

Tax Treatment

Since arbitrage funds invest 65+% of their assets in equities and equity derivatives, they are taxed like equity funds: 20% tax on STCG and 12.5% on LTCG. The gains also qualify for the annual ₹1.25 lakh exception limit for equity LTCG.

For folks in 30%+ tax bracket, the low risk profile and preferential tax treatment make arbitrage funds a more lucrative option than debt funds, and even high-yield bonds, which are far riskier.

Though future tax changes could make these funds less attractive, it’s unlikely that arbitrage funds will get a worse tax treatment than debt funds.

Liquidity

Arbitrage funds have a T+2 day redemption cycle, similar to equity funds i.e. if you trigger a redemption on Monday, you should get the money in your account by Wednesday. However, with weekends or bank holidays, it may take 5 days.

Comparison with Liquid Funds

Due to the safety profile and tax efficiency, arbitrage funds are often considered as a substitute for liquid funds. One must

- Risk

- Returns

- Tax Efficiency

When to select Arbitrage Funds

Arbitrage funds, by design, are one of the safest short-term instruments that you can put your money in.

The safety profile and favourable tax treatment make Arbitrage funds an exceptional choice for parking non-emergency funds. You can also use them for the portion of the emergency fund for which you don’t need instant liquidity.

Due to short-term fluctuations, it is advised to invest in arbitrage funds for 3+ months. This is also reflected in the exit loads of these funds as most them charge around 0.5% if you redeem with 15 to 30 days.

For instance, we park all our medium-term assets, which may be needed in less than 3 years, including our emergency corpus , in Arbitrage funds. We don’t use liquid funds because we use other means to manage immediate liquidity needs. We don’t invest in other debt funds either as their post-tax returns are only marginally better than arbitrage funds, but come with higher duration or credit risk.

How do I select Arbitrage Funds?

If you compare the historical returns of the arbitrage funds from top-tier AMCs, you would notice from picture #2 that the spreads between the performance of different funds have narrowed even significantly since 2023. The 2023 tax rules change brought in massive amounts of money into these funds forcing them into similar trades and pushing the returns to be more homogenous. The February 2026 change in regulations would tighten the spreads even further as there is even less left to fund manager’s discretion.

Given the limited room for differentiation within the category, large funds from well-established AMCs are all expected to perform similarly. While there will always be some performance differences between funds due to execution differences, it’s hard to predict the winners and likely the gap will be too small to matter.

At times, arbitrage funds can buy a stock on one exchange and immediately sell it on another, pocketing the difference. However, for most funds, such trading is a minor source of returns. ↩︎

“Categorization and Rationalization of Mutual Fund Schemes”, Feb 26, 2026 | SEBI Circular No.: HO/24/13/15(2)2026-IMD-RAC4/I/5764/2026 ↩︎

Subscribe For New Posts

Notes on money, tech, travel, and the occasional idea that does not fit neatly anywhere.

No spam, no market noise.